KEY LEARNING POINTS

- Councils should develop a good understanding of the typical financial challenges individuals and groups face, and the way funding is currently provided. They should build a thorough knowledge of the key lenders that are active locally, and the sort of projects they normally support, so, when they promote local initiatives, they can point private homebuilders in the right direction

- Group projects may be eligible for grant support via the Government’s Neighbourhood Planning programme or the Community Building programme. Build your knowledge of these programmes and advise local groups on how to apply. Some ethical lenders and charitable trusts are willing to provide finance for group projects. Understand how each of them operates, and the sort of help they can provide, so you can guide local groups

- Explore the financial solutions that have been developed in Europe to see if any of these can be adapted for use locally. For example a local lender may be prepared to introduce a new shared equity mortgage product, aimed at people on modest incomes (if you are prepared to act as a guarantor)

- When selling land, consider the scope to offer it on a deferred-receipt ‘Build Now Pay Later’ basis, and encourage other landowners to consider doing this too (this makes it easier for people on lower incomes to fund a project). Offering land on a leasehold basis also reduces the initial outlay needed, and creates a long term income stream.

- Councils could consider setting up their own revolving fund – to acquire land, service plots and then sell them. The proceeds can then be re-invested to create further opportunities

About

This is one of many Briefing Notes that explain resourcing, planning, land, finance, demand, marketing, consumer support and various technical issues. To see the full range of guidance click here.

Definitions

For the purposes of this Toolkit we have made the following definitions:

Click here to open/close

- ‘self and custom built homes’ are properties commissioned by people from a builder, contractor or package company (this is known as ‘custom build’ housing). When people physically build themselves, sometimes with help from sub-contractors, this is known as ‘self build’ housing. We call all these people ‘private homebuilders’.

- ‘serviced building plots’ are shovel-ready parcels of land with planning permission, laid out and ready for construction with access and utilities/services provided to the plot boundary. Some private homebuilders just purchase a plot; others opt for a ‘shell’ home (that they then finish off), or they select from an extensive menu of options offered by developers/builders.

- ‘group projects’ mean homes built by private homebuilders who work as a collective.

Statutory definitions are provided in

section 9 of the Housing and Planning Act 2016 which amends the Self-build and Custom Housebuilding Act 2015.

NOTE

This Briefing Note will be revised when the Regulations to support the commencement of the Self-build and Custom Housebuilding Act 2015 and the Government’s Right to Build policy are finalised.

Introduction

Many private homebuilding projects in the UK – especially group projects – find it challenging to secure finance. In Europe the situation is quite different and numerous innovative finance products have been developed, many of which may have the potential to be adapted or introduced here.

This Briefing Note outlines the UK’s current private homebuilding lending landscape, and it describes some of the innovative approaches developed in Europe. It also identifies most of the main sources of finance that are currently available here.

THE CURRENT LENDING LANDSCAPE IN THE UK

Mortgages for individuals

At present about half of all private homebuilders require some sort of finance to help them to fund their project. The other half are mainly older couples and families that sell existing homes to finance their new property.

In the UK individuals that require finance usually rely on a specialist self build mortgage. These mortgages release funds in agreed stages as the build progresses - the money is usually made available in arrears, with the finance transferred in five to six steps (depending on the method of construction). Typically private homebuilders draw down the initial stage when they buy the land, and then further finance is provided as their build progresses. Once the build is complete, many private homebuilders remortgage their property and take out a conventional mortgage.

Most of the 25-30 lenders currently active in the sector require at least a 10 per cent deposit, though some seek nearer 25 per cent. Interest rates are higher than standard mortgages (between 4 per cent-7 per cent), fixed rates and loan-to-value (LTV) ratios are also more limiting (average LTVs are about 60-70 per cent with the highest currently 90 per cent).

Self build mortgages are complicated to arrange and are therefore more expensive, with fees in excess of £2,000 not uncommon.

Some lenders will not fund the acquisition of land. If a private homebuilder is seeking funds to buy a plot lenders will normally require planning permission to be in place.

Default rates are low compared to conventional mortgages – roughly 0.5 per cent, compared to slightly more than 1 per cent for conventional mortgages.

The majority of the current lenders are small, locally-based building societies. Only one of the major High Street banks (Lloyds, via its subsidiary Halifax Intermediaries) presently lends to the sector.

Details of lenders who offer self build mortgages are available from a range of sources and can also be found here.

We believe around 5,000 self build mortgages are currently arranged every year in the UK, and that the average loan is in the region of £200,000-£250,000. Buildstore is the main broker that specialises in the sector, and we understand it currently secures £300-400m of funding each year, across a portfolio of lenders. The company often manages the process on behalf of the smaller building societies, helping applicants work out what they can afford, validating applications and project managing the stage payments.

Finance for groups

Raising development finance for group projects can be more challenging, as this niche sector is still evolving in the UK. Most mainstream lenders perceive collective projects as being more risky, as they involve dealing with a group of people.

There are, however, a number of specialist finance providers that are willing to fund group projects – for example Triodos, CAF and Resonance – and later in this Briefing Note we provide details of each of these (and several other potential sources of finance).

Groups sometimes ‘pool’ their financial resources (with the better capitalised members informally loaning money to those that have less); and groups are also exploring crowd funding as a way of generating the finance required to progress their project.

Government grants may be available to help groups progress their projects to planning permission stage (available via the Neighbourhood Planning and Community Buildings programme). Collective projects that include affordable housing can also apply for capital grant funding under the 2015-18 Affordable Homes Programme administered by the Homes and Communities Agency (but only for the affordable homes, not the whole scheme).

Many group projects access other Government funding streams too – for example land remediation grants, finance linked to alternative energy installations, the Custom Build Serviced Plots Loan Fund and the Neighbourhood Planning and Community Buildings programme.

For further information on the various Government programmes see our Briefing Note on

Government loans and grants.

TOP TIP

Build your knowledge of finance for the sector

Develop a thorough knowledge of the key lenders that are active locally, and the sort of projects they normally support, so you can point private homebuilders to the appropriate funders

THE UK COMPARED TO OTHER COUNTRIES

Europe

In continental Europe private homebuilders deliver a much higher proportion of all new homes, and hundreds of group projects are routinely built every year. The finance sector in Europe has responded accordingly, and more lending institutions provide finance – not just for individuals, but also to groups.

Councils across Europe, often working in partnership with banks, have also developed a range of specialist financial products to help people on modest incomes qualify for funding to help them to build their own homes.

In Germany and Holland banks don’t offer specialist ‘self build mortgages’ – they treat private homebuilders just like someone that would be buying a new home from a developer.

European banks and building societies don’t rate private homebuilding projects as being any riskier than any other form of house building. In Europe lenders typically offer a higher LTV (90 per cent is routinely available, and in some cases in excess of 100 per cent). Arrangement fees are also uncommon and charges are no higher than conventional mortgages.

In the Netherlands individuals can usually borrow up to 100 per cent of the market value of property, and in some cases more. The maximum loan is generally between four and five times the annual salary and typical interest rates are 3 per cent. Mortgages are tax deductible, so many people take out relatively large loans.

Individual mortgages for a group project are based on a standard stage payment finance product (the same mortgage that is used if buying off-plan from a developer).

In Germany most lenders offer flexible loans for private homebuilding and banks consider this form of finance an important part of their mortgage business. Loans are typically fixed for between 10 to15 years, although some can be for 20 or even 30 years. LTV ratios are typically between 60-80 per cent, interest rates range between 1 and 3.5 per cent with flexible repayments and limited or no arrangement fees. Top-up loans are also available under a Government assistance programme facilitated by the KfW Bank. This can provide up to €100,000 at fixed rates of 1 to 2 per cent over 10 to 30 years.

German banks usually set up a specific project account, and they use this to manage each loan to a custom or self builder. The main contractor responsible for delivering the home then submits invoices and self certifies that the required work stage has been completed. Typically there are seven to ten stages. Funds are paid directly to the main contractor as each stage is completed. Inspections by banks are only required where the build is considered particularly risky. In many cases up to 60 per cent of funds are released at wind and watertight stage with 5-10 per cent retained until completion. Experiences of defaults on this form of lending in Germany are extremely low - well below 1 per cent.

Over the last decade several European financial institutions have also developed well-proven products to support the rapid growth of group projects. For example, across Germany and the Netherlands there are hundreds of projects being built like this every year, and, between them they need access to development finance of hundreds of millions of Euro. So banks like Rabobank, GLS and the DKB have created bespoke financial products to meet the demand. Some cities are also providing funding, such as Hamburg, which is proactively supporting building groups.

A number of charitable foundations have also emerged in Europe to provide innovative finance for groups, such as the Trias Foundation – there is a mini case study on the Foundation’s innovative approach later in this Briefing Note.

MINI CASE STUDY - DE FLATS, AMSTERDAM

The community organisation that coordinated this 500 home ‘self refurbishment’ project arranged for two banks to provide financial advice to would-be purchasers. The banks – ABN AMRO and Triodos – set up temporary ‘pop up’ facilities in converted shipping containers so that would-be purchasers could meet representatives in the evenings and weekends when they were visiting the site. At these meetings the banks provided advice on mortgages and loans. Potential purchasers were asked to bring copies of their bank statements, and the banks agreed to evaluate their income and make an offer on any loan they might need to fit out their property (refurbishment works typically cost between €10,000 and €20,000). The banks also calculated how much mortgage finance they could offer to help people to then buy the homes on a long term leasehold basis, as is common practice in Amsterdam.

North America and Australia

Similar funding models can be found in the USA, Canada and Australia.

In the

USA ‘Home Construction Loans’ and ‘Lot and Land Loans’ are readily available. However, to protect them from risk lenders generally impose strict qualifying requirements and applications are rigorously assessed, and most US lenders require people to work with a qualified/reputable builder or contractor.

LTV ratios are typically around 80 per cent with interest rates normally 1 per cent higher than conventional mortgages, which are currently at around 3 to 4 per cent. Fixed rates between 10 to 30 years are possible. Construction Loans are short-term development finance loans (usually 12 months) and are paid off as soon as the house has been completed. Interest is charged on funds drawn down in pre-agreed stages with the lender. Most lenders allow an extension if this is necessary.

Construction-to-Permanent loans are also commonplace and are available at better rates. Under these the initial construction loan converts to a mortgage on completion. The construction loan incurs interest-only payments; the conventional repayment mortgage typically has a fixed rate over 15 years.

To help borrowers with their cash flow, construction loans can be structured with an interest reserve fund. This is where the lender agrees to set aside a proportion of the agreed loan to relieve the borrower’s monthly obligation to make the required interest payments during the build – at least until all of the funds in the interest reserve have been used. The reserve may be structured to cover all or only part of the expected interest charges, depending upon the lender’s rules.

Most new housing in

Australia is delivered by property developers, working on behalf of private homebuilders. The developers acquire land (once it is zoned and released for housing), they service the land, and then either build homes and sell them as a complete house and land deal, or offer a number of standard or customisable home designs.

There are three main ways of financing a private homebuilding project in Australia: -

- House and Land Packages

- Construction Loans

- Owner Builder Mortgages (for self builders)

Of the 111 lenders on Australia’s main financial comparison website, 86 offer one or more of these options.

House and Land Packages

Financing for a House and Land Package usually consists of two elements - the first is a loan to purchase the land, and the second a construction loan. Loans can be arranged separately, but are usually bundled. LTV ratios are typically around 80 per cent with interest rates normally about 4 to 5 per cent, and these can be fixed for 10 years.

Most finance providers lend 60 - 65 per cent of the value of the land (but 90 - 95 per cent loans are available), plus the construction costs.

Off-plan sales and House and Land packages usually have different finance plans. Commonly, private homebuilders pay a 5 per cent deposit on the land and the house, but deferred payment options are sometimes available. There are also some 100 per cent, or ‘no deposit’ financial products available for the construction part of the loan.

Construction Loans

Construction loans are available to cover the building cost of a home. Almost all construction loans are set to interest-only payments, drawn down in pre-agreed stages with the lender. Staged valuations are common at slab, wind/watertight and completion stages. Payments follow an agreed schedule with the builder forwarding invoices to the bank, which then reimburses them direct. Once the final payment has been made to the builder, the loan becomes a standard repayment mortgage, or a homeowner can remortgage.

Applicants are required to have a signed contract with a licensed builder, and lenders often ask for an agreed fixed-price building schedule. Builder risk insurance and extra fees to cover valuation costs are standard and are in addition to regular upfront fees such as application costs. All builders in Australia are required to have adequate insurance to cover against insolvency.

Owner Builder Loans

Owner builder loans are available for private homebuilders who want to self build their own home without engaging a licensed builder. To do so they need an owner builder license and must complete a recognised course. Anyone can become an owner builder but there are different guidelines set out for each Australian state. Owner builder loans can be complex and difficult to secure. The maximum LTV available is 80 per cent, and this is only available from a few lenders. Most lenders will generally accept 50 - 70p er cent LTV. Lender normally require a robust cost estimate and a contingency of 10 to 20 per cent of the build cost.

TOP TIP

Learn from abroad

Explore the financial solutions that have been developed overseas to see if any of these can be adapted for use locally

SUPPORT FOR BUILDING GROUPS IN THE UK

There are a number of sources of potential finance for groups. The following ethical lenders and charitable trusts are currently most active in supporting group private homebuilding projects:

Triodos Bank and Triodos Investment Management

Triodos Bank has a track record of supporting socially or environmentally progressive development projects, including community-led housing. On occasions the bank is willing to take a long-term view on the return on its investment, and this has been very helpful for group projects that want to build homes for affordable rent.

Triodos Investment Management is willing to take an equity stake in some projects, which can also be another way of funding a development. Further information is available here.

CAF Venturesome and CAF Bank

CAF Venturesome provides access to finance for organisations with a clear charitable or social agenda. Between 2002 and 2015 it invested more than £36m across almost 500 organisations.

It often provides unsecured loans (where other lenders cannot) via its Social Impact Fund. Loans of between £25,000 and £350,000 are also available to help with working capital and cash flow gaps. CAF offers a ‘standby facility’ – similar to an overdraft for community groups; and a range of less common social investment products, including Social Impact Bonds and revenue participation agreements.

CAF Venturesome established the Community Land Trust (CLT) Social Investment Fund to support community land trusts. This Fund provides pre-development loans of between £20,000 and £60,000 – conventional interest is not charged, although a 25 per cent ‘success fee’ is levied on all projects that proceed.

The aim of the Fund is to get projects off the ground and encourage other lenders to enter the sector. It provides development finance of up to £350,000, typically with 6.5 per cent interest and on a 20-40 per cent LTV ratio, as long as there is a commercial finance provider involved in the project. A report on its experience of lending to community groups is due in early 2016.

Further information is available

here.

Ecology Building Society

The Ecology Building Society has a strong track record of providing stage payment self build mortgages for people constructing their homes to a high ecological specification. It also offers long-term mortgages to community groups that need to pay off development loans. Further information is available here.

Resonance

Resonance matches socially-motivated investors with social enterprises that need finance. It also provides investment-readiness consultancy, and helps groups to launch community share issues, or find other investors. Its Community Share Underwriting Fund (CSU) underwrites asset-backed community share issues up to 50 per cent of the project’s fundraising target. Further information is available here.

Big Issue Invest

The Big Issue Invest programme provides loans of between £50,000 and £1.5million through its £10m Social Enterprise Investment Fund. These loans are available for community-led development projects with high social value or low environmental impact. Further information is available here.

Power To Change

The Big Lottery-funded ‘Power To Change’ programme provides grants of between £50,000 and £500,000 to community businesses in England. To be eligible group projects must demonstrate an element of community control and positive social, economic or environmental outcomes. As of October 2015, Power To Change offered an Initial Grants Programme. In early 2016 this is expected be replaced by a longer-term grants programme. The Fund has around £150million to invest over ten years. Further information is available here.

Tudor Trust

The Tudor Trust is an independent grant-making trust that supports smaller voluntary and community groups with core funding (to cover salaries, etc), project grants (to support project development costs) or capital grants (to pay for land or buildings). In 2013-14 it provided 365 grants worth almost £20m. Further information is available

here.

TOP TIP

Specialist lenders

A small number of UK based ethical lenders and charitable trusts provide finance for group projects. Understand how each of them operates and the sort of help they can provide so you can advise local groups on how to apply

WHAT CAN COUNCILS DO TO HELP PROVIDE FINANCE FOR PROJECTS?

Councils who want to support local people that want to build their own homes can help by: -

- Signposting private homebuilders who need a mortgage to the most appropriate lenders that are currently active in their local area

- Engage with organisations such BuildStore - currently the UK’s largest self build mortgage broker. Cherwell District Council refers many of its would-be private homebuilders to the company so they can check what level of finance they may be able to raise.

- Develop a partnership with a lender, whereby they act as a mortgage guarantor for those on lower incomes who need a mortgage to fund their build. Councils can facilitate mortgage finance themselves, for example by joining the Custom & Self Build Scheme (see box below)

- Set up a modest ‘self build revolving fund’ to bring forward serviced building plots or land to support group projects. For example Teignbridge District Council has allocated £1m to a fund like this – to help it buy land, that it will then sell as serviced plots (with the income from the sales being recycled to enable it to deliver more opportunities)

- Work closely with local housing associations, housing co-ops and charitable foundations to see if they can collectively provide financial support to viable projects

- Where the council is selling land, consider the scope to offer this on a deferred-receipt ‘Build Now Pay Later’ basis. You may also be able to encourage other landowners to consider this too. For small developers and people on modest incomes this can be very helpful, as it means they won’t have to finance the purchase of the land at the start of the project. Birmingham City Council’s deferred receipt model is a good example. Using this model the council does not receive payment for the land up front. Instead it enters into a legal agreement with the developer to defer the land receipt for up to three years, with an associated profit-sharing arrangement for the overall development profit. The Government has published an explanatory note on the use of deferred receipts that is available here.

- Consider making land and plots available on a leasehold basis. This helps smaller builders and people on lower incomes as it reduces the up-front cost of land. In cities like Amsterdam and The Hague many of the plots are sold this way, and the annual leasehold rental provides a steady income stream for the council.

TOP TIP

Revolving funds

Consider setting up your own revolving fund – to acquire land, service plots and then sell them. The proceeds can then be re-invested to create further opportunities

TOP TIP

Leasing land

Explore providing leasehold building plots, as this reduces the initial outlay for people on lower incomes, and small builders. The annual leasehold rental can provide a steady income stream for a council

TOP TIP

Build Now Pay Later

Investigate selling land on this basis – it makes it easier for the people on lower incomes to fund a project

THE CUSTOM & SELF BUILD SCHEME (CSB)

Capita Asset Services has developed this scheme in association with Lloyds Banking Group. It is designed to help councils work in partnership with residential mortgage lenders and developers to offer access to more affordable mortgages for private homebuilders, either on their own land or on privately owned sites.

The scheme is based on the existing local authority mortgage scheme (LAMS) and is designed to de-risk the process of obtaining mortgages for privately built homes.

How does it work?

The scheme is for councils that: -

- Have land for development

- Are in the process of leading a development

- Are working in partnership with a developer

Once plots are available and a site is marketed private homebuilders can apply under the scheme for a mortgage from a panel of lenders. Once the mortgage is approved the private homebuilder pays a 5 per cent non-refundable deposit that the council receives. The council then funds the cost of the agreed build to completion, at which point the mortgage is provided by the lender and the build costs, including interest, is paid to the council. The private homebuilder will then take ownership of the property and commence mortgage repayments.

The scheme is available to all private homebuilders that can afford mortgage repayments and have at least a 5 per cent deposit. Councils can set the maximum limits for the mortgages they are willing to support under the scheme, and these are agreed with the mortgage lender at the outset.

What are the benefits?

- Councils can support local private homebuilding opportunities and can potentially facilitate a mortgage early in the development process

- Private homebuilders can access higher LTV mortgages (up to 95 per cent), making private homebuilding more accessible

- Councils can release land for private homebuilding but retain overall control until a home is completed. This reduces the risks associated with traditional self building, such as cost overruns, delays and non-completion, as the council retains ownership of the property until completion at which point it recovers its costs as the mortgage completes

- There is no need to make stage payments, making lending as straightforward as a traditional new build mortgage

- Councils get operational support in administering the scheme

Points to be aware of

- Councils will need to finance the majority of the costs, which are recovered (with interest) on project completion

- Councils will need to work in partnership with developers to commission the construction of homes and engage directly with private homebuilders

The rest of this Briefing Note showcases some of the interesting financial initiatives that have been developed in Europe. Many of these have potential to be adapted to the UK market.

THE ‘I BUILD AFFORDABLE’ INITIATIVE IN ALMERE (IbbA)

The IbbA provides a ‘top up’ loan to help people on modest incomes boost the amount they can borrow, so that they can then afford to build a simple, modest terraced property.

More than 500 families have been supported by this initiative over the last six years and it has proven to be an effective way of delivering ‘intermediate’ private homebuilding. Key points to note are: -

- The scheme is only available to those on modest incomes – £19,000 to £30,500 – and it provides a ‘top up’, interest free loan (for an initial three year period) to enable people to purchase a cost effective terraced property from a catalogue of more than 40 different house types

- Purchasers can select the house design they want and make minor internal adjustments. The construction and price of each home is then guaranteed by a qualified builder who then builds it

- A typical three bedroom home (95 sq m) costs £75,000 to construct, plus the cost of the plot (£28,500). A range of larger homes is available (the biggest is 143 sq m which costs £92,000)

- The initiative has been so successful that it is now being rolled out across a number of local authority-led private homebuilding developments in the Netherlands

HOW DOES THE SCHEME WORK?

The IbbA was set up by the city of Almere in partnership with deKEY and Ymere (two social housing providers), and independent financial partner SVn (a public sector bank that specialises in funding affordable housing initiatives). The scheme is financially neutral, so it is not designed to make a profit.

In The Netherlands there are ten conventional banks that provide mortgages, usually up to a maximum of four times of a private homebuilder’s income. For example a household earning the equivalent of £20,000 a year can get a mortgage of £80,000.

The challenge however is that even with a cost effective house type and an economic (100 sq m) plot, the

total cost of a house is more than this. The IbbA therefore provides a top up loan to cover the difference.

The top up loan is interest free for the first three years. If the homeowner’s income has not increased over this period the loan remains interest free. Where income has increased they then have to start to pay the interest (charged at a fixed rate of 4.1 per cent over 15 years) and, if they can afford it, also some of the loan repayments. The 4.1 per cent interest rate is slightly higher than normal (3.8 per cent). The private homebuilder’s income is assessed again at regular intervals with repayments usually adjusted upwards (provided they can afford increased repayments).

The size of the top up loan is limited to no more than 40 per cent of the total market value of the finished home.

For example if a simple terraced house costs £75,000 to construct and the plot costs £28,500, the total finance required will be £103,500. The finished property will have a market value a little higher than this – typically around £110,000.

A household with an income of £20,000 will be eligible for a £80,000 mortgage. So the top up loan they need will be £103,500 minus £80,000 = £23,500. This is 21.3 per cent of the final value of £110,000, so well below the 40 per cent threshold.

In fact a family earning £20,000 a year could potentially afford a new property valued up to £134,000 (as the maximum they could borrow for the top up loan, in addition to their £80,000 mortgage, would be £54,000 or 40 per cent of £135,000).

At present the typical top up loan is £35,000. As there are roughly 100 IbbA homes a year being delivered, the total value of the loans is roughly £3.5m a year.

SVn has secured finance for this very straightforwardly, as it has the city of Almere and two housing associations backing the initiative, and they all have excellent credit ratings.

WHAT IF A PRIVATE HOMEBUILDER WANTS TO SELL THEIR PROPERTY?

If someone needs to sell their property, it is valued and the mortgage and the loan is repaid. If the property has increased in value the uplift is also used to pay off the interest that would have been charged on the top up loan.

If there has not been much of an increase in the property’s value, and there is not enough available to pay all the interest that is owed this shortfall is picked up by a National Guarantee scheme run by the Government. All the purchasers have to pay 1% of the price of their home into this Guarantee Fund to help provide cover for this eventuality.

The IbbA and the city council also constructed a useful ‘financial reserve’ that it can use to help minimize the risks associated with the project. When the council sells a plot to the IbbA it initially sells it at a discounted price (the same price as it would sell the land to a housing association). In Almere’s case this is around £15,500 per plot. The homebuilder pays the full market price (£28,500) for the land. The difference – roughly £13,000 per plot - is held in a reserve fund in case there are any unforeseen financial difficulties during the project.

During the initial set up phase the city council underwrote the cost of establishing the IbbA team. Now, with more than 100 homes a year being built, all the operational costs are comfortably covered.

HOW DO THEY ACHIEVE SUCH LOW CONSTRUCTION COSTS?

The IbbA team organised a competition challenging building contractors and architects to come up with designs that could be built for a maximum of €125,000. As part of the competition rules the entrants had to be willing to guarantee the cost/specification of the home, the timescale to build it and its energy performance.

The IbbA scheme provides top up loans on starter properties like these. None costs more than €125,000 to build. There are more than 40 house types (and many options to customise them), and each contractor guarantees the cost of construction

The IbbA scheme provides top up loans on starter properties like these. None costs more than €125,000 to build. There are more than 40 house types (and many options to customise them), and each contractor guarantees the cost of construction

Almost all of the homebuilders who have used the IbbA’s top up loan have selected one of the homes from the IbbA’s catalogue, and it is clear that some designs are more popular than others.

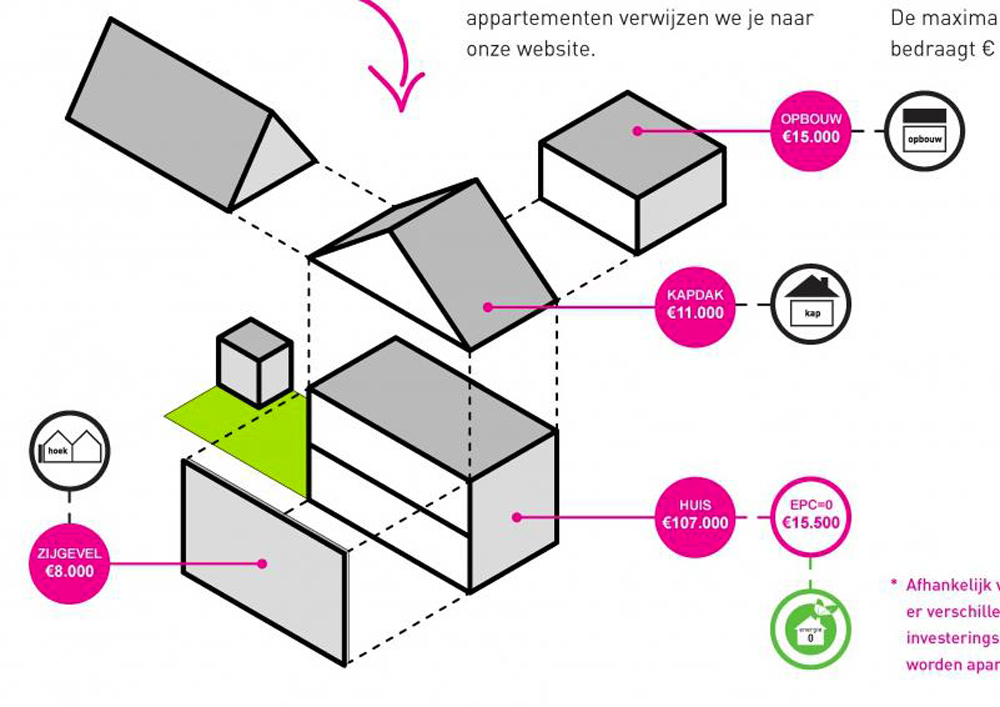

Very clear basic information is provided to help guide potential homebuilders on the cost implications of different designs and layouts. For example the additional cost of an ‘eco spec’ home, the what it costs to go from a two story home to a three storey property

Clear guidance is provided to show the cost impact of adding features to a home – for example an extra floor adds €15,000, a separate end (or party) wall add €8,000

Clear guidance is provided to show the cost impact of adding features to a home – for example an extra floor adds €15,000, a separate end (or party) wall add €8,000

People are also allowed to use the IbbA to fund a bespoke solution via their own architect/builder team – but only three of the homes have so far been delivered this way.

WHAT DO PRIVATE HOMEBUILDERS HAVE TO DO?

Once their funding has been approved they are expected to oversee and control the construction process. They also have to commit to make the loan repayments, and there is no flexibility on this. So, for example, if a couple separate or one of them looses their job or is off work for a long period, they still have to make the repayments. This applies throughout the 15 years of the loan agreement, even towards the end when the repayment regime will be more costly.

One of the conditions of the IbbA is that homebuilders have to hire a pre-approved technical/building coach to help them. The coaches’ fee is just over £2,500 per house. Their job is to advise the homebuilder about all the technical, contractual and other issues they will encounter.

THE ROLE OF THE TECHNICAL/BUILDING COACHES

All of the IbbA homes are terraced properties, and one of the things the coaches try to do is co-ordinate the ground works, foundations and party wall construction along the terrace – usually they try to build 10-15 homes at one time in an informal group. The use of party walls (instead of two separate walls with a small gap) has a big impact on the construction cost – saving about £6500 per home, and creating a little extra internal space too.

The contractor’s price includes a basic kitchen, and delivers a complete building that is ready to occupy. However, private homebuilders have the flexibility to reduce the total cost and fit their own kitchen and do other minor works if they prefer to do it, but only after the main contractor has moved off site. The coaches play an important ‘guardian angel’ role in ensuring the main contractor’s work is done on time and to the right standard, and they also monitor the homebuilder to ensure any fitting out work meets local standards.

The coaches also agree the stage payments to the building contractor. All the funds (mortgage and top up loan) are made available when construction work begins. This is when the plot purchase technically happens. Usually 5 per cent of the contractors’ total cost is withheld until everyone is satisfied with the contractor’s work. For more information on the role of coaches see Briefing Note

Support and training for individuals.

Most of Almere’s technical/building coaches are people who have a strong track record in construction

Most of Almere’s technical/building coaches are people who have a strong track record in construction

Homebuilders can choose to do more of the construction work themselves, but their coach, the building contractor and the IbbA team have to agree this in advance. In reality very few opt to do this.

The biggest problem is construction delays – 20 per cent of the homes are three to four months late. Homebuilders are incentivised to finish on time, and they can face a penalty if their home is delayed. However, the IbbA team says penalties are seldom imposed as these just put the private homebuilder into deeper debt.

What other support does the IBBA provide?

Initially the IbbA team spends a lot of time with each potential purchaser, explaining the process, evaluating their income and pre-agreeing the loan etc.

Once a loan is approved the team also arranges five meetings for all of those involved in the construction of a new group of homes (typically 10-15 properties): -

- The first meeting is when people choose their plot, and ‘speed date’ with the pre-approved technical coaches that are available, to find the one they feel most comfortable working with

- The second session focuses on any planning or other permits that will be required, the construction process, the timeframe, and any questions

- The next meeting involves working closely with their neighbours to resolve any technical issues over party walls, or awkward ‘junctions’ (for example a two storey home could be built next to a three storey one; or a balcony might clash with an overhanging roof on the neighbour’s house). The building coaches play a key role in reconciling any issues or conflicts

- The fourth session focuses on finance, and gives everyone a chance to double check they are on budget and have their finance all in place

- The last get-together coincides with construction work beginning on site. This is usually also an opportunity to celebrate the progress that has been made

How is the IBBA structured?

The IbbA team is made up of four staff (one manager, one legal expert, one finance expert, and one technical expert). Administrative back up is provided by the four strong reception team at the Almere Plot Shop. The support from the Plot Shop team is recognised with a payment of around £2,500 per home towards their overheads.

RABOBANK’S SUPPORT OF GROUP PROJECTS

Background

Rabobank is a Dutch multinational banking and financial services company headquartered in Utrecht in The Netherlands. The group comprises 113 independent local Rabobank branches, a central organisation (Rabobank Nederland) and a large number of specialised international offices and subsidiaries. It operates in 40 countries with 47,000 staff and 8.8m customers. Its profits for the first half of 2015 were €1.52bn.

The bank functions as a federation of cooperative associations. Each of these associations has considerable autonomy.

Revolving fund in partnership with local councils

One of the branches has developed a financial initiative to help the growing number of building groups that were emerging across the country. The bank was interested because it wanted to: -

- Sell more mortgages

- Access new business in areas like Almere (where new homes are built predominantly by private homebuiders)

The initiative involves establishing a revolving fund in partnership with a local council. This is then used to help ‘pump prime’ and support groups in their early stages of project development.

Each ‘revolving fund’ is slightly different and in most cases both the bank and the council initially make a financial contribution (though Rabobank has, on occasions, been the only contributor). In some cases, no interest is charged on the loans used to set up the fund (for example in Almere). In other situations, where a council needs to generate a small return, the fund pays a little interest to both parties.

The benefit of a revolving fund is that it establishes a partnership between the bank and a council with benefits for both parties. The council is seen to be acting to support and encourage group projects and the bank benefits from increased mortgage business.

How does financing work?

The fund helps groups by providing advance loan finance for each member. This money can be used to pay for professional help, to establish a business plan, to get the group legally constituted and to cover professional fees to design the project.

Key conditions and scale of funding include: -

- The fund will loan up to 60 per cent of required finance and is capped at €20,000 per member (ie €12,000 from the bank, €8,000 from each individual)

- Groups have to be legally constituted with agreed rules and contractual obligations

- Groups must be democratically controlled (not just led by one or two directors)

- Groups have membership limits (groups with more than 50 members are likely to not be supported)

- Groups must employ a ‘Process Advisor’ to help with the establishment of the group and to prepare a business plan. The advisor will also work with each group member to assess what additional finance they can raise towards the project. For more information on the role of process advisors see Briefing Note Support and training for individuals.

Before a group can get formal funding for its development it has to have secured an option on the land.

When the group has prepared everything that is needed it then seeks approval from the lender for a loan to pay for the overall building work. This is repaid in full with interest when the individuals take out their mortgages on their homes. As the mortgages are drawn down before the work starts, they effectively fund the construction work. The mortgages also repay the advance finance loaned to the members from the revolving fund. The fund cab then be recycled to support another group project.

Group members are free to take out a mortgage with other banks, but most opt to use Rabobank as it has, by then, developed a close working relationship with everyone.

Rabobank considers that the advance finance it offers from its revolving fund accelerates the group formation and project implementation process. Groups that the bank has supported are usually able to get on site within 12-24 months (this is much faster than groups that are unsupported).

The bank normally considers there to be three broad stages to group projects: -

- Initiation stage – when groups form and decide what they want to achieve

- Design/Development stage – when a site is identified and drawings for the project are prepared and approved

- Build stage – when construction finally starts

Process Advisors

The bank believes process advisors are critical to the success of any group project and that they reduce risk for the lender. Banks in Germany share this view.

Rabobank believes a good process advisor needs to: -

- Know how the planning system operates and how legislation works at local authority level

- Understand the political processes within a local community, as they have to keep the wider community/neighbours on board

- Mediate between different group interests and help with decision-making in a fair equitable way, avoiding conflict between group members

- Really listen to the group

Rabobank does not consider architects to generally be good process advisors. It also not considered essential for a process advisor to be an expert quantity surveyor as this service can be commissioned by the group.

Expansion plans

Rabobank allocated €400,000 to its first revolving fund for Almere. This is the bank’s largest fund as Almere is one of the biggest and fastest growing cities in the Netherlands, and the council supports group projects. So far seven projects (varying in size from 19 to 44 homes) have been enabled through the fund, providing a total of 176 homes.

The bank is currently creating new funds in partnership with several other councils. The first four are at: -

- Wijk bij Duurstede – this fund has €120,000, and its first project will provide 27 houses

- Nieuwkoop – €100,000

- Delft – €200,000

- Rijswijk – €200,000

Rabobank is also working with the city of Nijkerk to set up a fund of about €180,000, and it has agreed to establish funds in association with the provinces of Groningen and Drenthe.

THE HAMBURG INVESTMENT AND FUNDING BANK (IFB) MODEL

Background

The City of Hamburg supports the finance of group projects through the Hamburg Investment and Funding Bank, IFB Hamburg.

The IFB was launched in 2013 to provide finance for residential construction, business development, innovation and environmental or climate protection projects. It acts on behalf of the City of Hamburg and is the central organisation for support funding by the council. Its activities target inward business investment and aim to strengthen Hamburg’s position as an economic location, including helping the council implement its housing objectives. It has allocated €717m of prudential equity and has so far funded 2,410 group built homes worth about €123m.

What can be funded?

Funding is available to legally constituted groups who want to build homes for their own occupation. Groups typically have between three and 20 households.

The members form themselves into a recognised legal entity that can contract with builders, architects, project managers and apply for funding, land acquisition and planning permission.

Three legal entities are eligible to apply for finance from the IFB: -

- Private home ownership groups - where the individuals each own their own home

- Cooperative ownership - where the individuals that form the cooperative all have the right to the use of a home

- Groups of individuals that are supported by an established cooperative.

In England a legally constituted group would typically be a Community Land Trust, a housing cooperative, or a community group recognised under the 2011 Localism Act.

To be eligible to apply groups must be registered with Hamburg’s Agency for Building Groups. The agency checks if a group is legally constituted and whether it meets the required funding criteria.

Hamburg regularly identifies parcels of land for groups to acquire. Once a group has been selected to purchase one if its sites the council enters into a 12 month ‘exclusivity contract’. This gives the group time to arrange funding and secure other permissions. Groups are required to pay 1% of the purchase price when they sign the exclusivity contract, and they can then apply for funding to the IFB. Groups purchasing land on the private property market require a legal option on the land to be eligible to apply. They must also be registered with the agency.

The IFB provides advice to groups ahead of preparing an application, particularly regarding their creditworthiness. It has also published comprehensive guidance for applicants entitled ‘Building Groups: funding guidelines for building groups with co-operative ownership’.

Funding is administered in the form of a repayable loan with low interest rates over 20 years (30 years are also an option). Groups can structure the loan from a number of different funding elements: -

- Basic loan for land purchase and construction works (this is a mandatory element)

- Low-interest fixed-term loan of up to €50,000 per home to encourage energy-efficient construction - this is available under the national KfW (the German government-owned development bank) programme.

- Funding for car parking

- Supplementary loan funding where required, depending on the project

Groups can also apply for grant funding for a number of different funding elements: -

- Small scale income-related grants for households

- Funding for the creation of lifetime homes, inclusion of lifts, energy efficient construction and use of bricks in refurbishment projects (where required for conservation projects)

Scale of loan funding

Land purchase: -

- For non-council owned land, up to €800 per sq m. This amount can be exceeded up to the value of the site and can be applied for retrospectively if the site was purchased within five years of the application for funding

- For council owned land, up to €600 per sq m (maximum)

- Loan cannot exceed 50 per cent of land cost

Construction: -

- New build housing for rent by co-operatives, €1,200 per sq m for first 1,500 sq m total floorspace and then €1,100 for every additional sq m of floorspace

- Loan cannot exceed between 80-90 per cent of total build cost

The annual interest rate is 2 per cent which is fixed and arrangement fees of 0.25 per cent per month are payable for funds which have not been drawn down after six months of the loan being agreed. There is also an administration fee of 1 per cent of the agreed loan.

Loans must be accepted within 18 months of offer, and the loans are secured as a first charge on the property.

Hamburg’s Agency for Building Groups has prepared this summary of the funding that is available to groups

Hamburg’s Agency for Building Groups has prepared this summary of the funding that is available to groups

Eligibility criteria and fund administration

A group will need to provide documented proof that it is supported by an independent ‘building coach’ (Baubetreuer), and a registered architect. Where a group works with a co-operative, the co-operative can fulfill the role of the building coach.

Groups must also submit proposals that illustrate the broad concept and number of homes proposed (not outline planning permission). The homes must, on average, be between 40 sq m (for one person) and 120 sq m (a six person household. There are also exceptions for households with children. Communal space is funded at €1,200per sq m but cannot be larger than 2 sq m for every home built.

The homes must meet specified energy efficiency standards.

Households with annual gross incomes between €18,000 and €97,000, and any property that is built for rent, must have an open rental agreements (no limit on the end dates).

Funding is administered by the IFB. Applications must be made before the start of building works and are rigorously assessed for due diligence.

The loans are in the form of stage payments agreed with the IFB. They broadly follow the build stages of a project and are paid in advance. Repayments must be made quarterly and amount to at least 2 per cent of the loan per year plus interest.

Applications from groups require a legal contract outlining how the ownership is divided among members, either as a co-operative or as individual home owners. This will inform the structure of the loan.

Where applications for funding are unsuccessful, a new application can be made after six months from the decision date. There is no scope to challenge funding decisions.

THE TRIAS FOUNDATION AND THE GROUND LEASE MODEL

Background

Trias is a socially-oriented foundation (or ‘Stiftung’

) based in Hattingen, near Dortmund in Germany. It operates nationwide and is primarily involved with self-organised housing projects. Its main objective is to channel commercial expertise towards social aims, by ‘capturing land value’ through purchasing land, and then leasing it on to housing organisations via a 99-year ground-lease.

Foundations in Germany generally operate as investment trusts – and typically buy shares in companies in order to generate an income stream to fund their social objectives. Trias has chosen to buy land to generate its income. By opting for this approach is can also support projects that fit with its social and environmental objectives.

Investment fund

The foundation was established in 2001 with an initial capital fund of €70,000 raised from around 20 socially-motivated private individuals, each gifting varying amounts. This included a network of finance and development professionals who were interested in seeing more of these projects happen.

The Foundation generates an income from its investment in land through an annual ground rent of 4 per cent of the purchase price. In this way, the foundation is able to strengthen itself through each project it supports. By 2015 its fund had grown to be worth around €7.5m.

Trias is often able to secure sites at a discount, as landowners like to be associated with its good work supporting worthy housing projects. The foundation also brokers investment in projects from philanthropic investors, or from other foundations who see its work as being more ethical.

Other support for groups

The foundation’s reputation – largely underpinned by that of its Chief Executive, former banker Rolf Novy-Huy – also means that other stakeholders are confident about a project’s viability if Trias is involved. For example, a council can be reassured that a site sold at a discount will be protected by the Foundation’s ground lease rules. Lenders such as GLS Bank can also be confident a project is viable by virtue of the fact that it must be able to pay Trias’ annual ground rent.

The Foundation also supports groups that want to build their own homes by providing information and resources – such as model contracts, legal constitutions and tax advice - and by brokering access to expertise and commercial finance. Trias sees the provision of a robust information service as a core part of its work.

To further support this aim, the Foundation set up and maintains the

www.wohnprojekte-portal.de website, which lists details of self-organised housing projects all over Germany. It licenses its database for use by other organisations and is soon to introduce an English language version of the site in response to interest from abroad.

How does financing work?

If a site is priced at €300,000 Trias might initially suggest that the group has to raise €100,000 itself, through member deposits or membership fees. Trias will then invest €100,000 of its own capital funds (effectively as a donation), and will also broker a further €100,000 loan from a private individual or another foundation, which it then repays through its ground rent on the land. Once the loan has been repaid, the ground rents revert to Trias to build up its investment fund.

Type and number of projects supported

Trias will support projects that have a similar social or environmental aim as those of the Foundation. It prefers refurbishments rather than new projects, but will support new-builds on brownfield sites.

To date it has supported 28 projects (that have collectively provided 330 homes) since 2001. The organisation is particularly active in Berlin, and in the Ruhr valley where it is based.

Although the Foundation focuses on cooperative projects, it will also support private groups (‘Baugemeinschaften’). Groups do however need to be promoting sustainable lifestyles to be supported.

Trias prefers groups if they have the support of another stakeholder, such as a council or a bank.

The Leuchtturm e.G project in Berlin is one of 28 projects supported by Trias since 2001

The Leuchtturm e.G project in Berlin is one of 28 projects supported by Trias since 2001

Staff, Skills and Resourcing

Trias generates approximately €400,000 a year in ground rents from its current land investments. It spends roughly 50 per cent of this on its operational costs, with the other 50 per cent granted as gifts to other similar non-profit organisations.

The organisation is run by two full-time and two part-time paid staff – the equivalent of three full timers. Annual staff costs are about €80,000. It is governed by a Board of Directors that receive no remuneration other than expenses.

Updating and maintaining the Foundation’s project information portal requires between 0.5 and 1 person full-time and a budget of €5,000-10,000 per year to cover technical costs. The initial set up cost for the portal was about €50,000.

HOW THE GLS BANK FINANCES GROUP PROJECTS

Background

The GLS Bank (GLS Gemeinschaftsbank eG) is a large German co-operative bank that was founded in 1974. It was the first ethical bank in Germany and it focuses on cultural, social and ecological initiatives. It has to date financed around 23,000 initiatives and businesses. Loans are offered to projects such as schools, organic farms, nursing homes and a range of renewable energy businesses. Since 1990 it has also financed nearly 300 group projects of between 10 and 35 homes.

Although GLS is a member of the Global Alliance for Banking Values - an independent network of ethical banks - it does not operate outside of Germany.

In 2014 GLS issued loans of €2bn, of which €400m was allocated to residential developments. This included €100m for building groups providing rented accommodation and €100m for owner occupied building groups. The bank is growing and its loan exposure to group projects is expanding due to increasing demand.

Building Group profiles

The bank lends to building groups that plan to rent or own their properties. Rentals are often refurbishment projects. Ownership projects are typically new-build. In the bank’s experience building groups fall into two broad categories: -

- Younger groups - where members are typically under 50 years of age, well-educated and have more time for meetings, but have less capital. The bank finds them easier to work with as they are willing to listen to advice and are more used to working together. They can also have a higher borrowing potential than older groups

- Older groups - where members are typically 50 to 70 years of age. These groups tend to be better capitalized, but may struggle to get a mortgage due to their age. They are less likely to accept advice from the bank and can be less cohesive as a group

Interest rates and fees

GLS’s objective is to keep interest rates as low as possible for building groups – typically around 2.25 per cent (slightly lower than commercial developers can expect), and it does not charge an arrangement fee, valuation fee or for any initial advice.

Interest rates are fixed for either five or ten years. Overpayments in excess of agreed monthly repayments can be made up to €5,000 per year at no additional cost.

Approach to risk and defaults

GLS pro-actively manages the risks associated with group projects prior to agreeing any funding by requiring groups to: -

- Be legally constituted as a limited company (for the ownership model) or as a non-profit organisation (for the rental models)

- Appoint a single point of contact in-house for liaison with the bank

- Appoint a project manager such as an architect, surveyor or other qualified professional

- Have between 10-30 per cent of their own capital which they have to pay into a group payment account held by the bank in advance

The bank also thoroughly assesses the viability of projects and, if needed, advises groups to adjust their project prior to determining an application for funding.

When a group plans to rent its homes the bank requires the group to set up a company into which the rents are paid. The group is then responsible for paying off the loan, and for the long-term management and maintenance of the project. GLS often works with non-profit foundations and trusts to spread the risk on affordable rental-model projects. It also prefers these projects as they fit with the bank’s ethical objectives.

Ownership projects are also required to set up a company – but this is only required for the construction phase. Funding is administered in the form of mortgages for each member of the group, which is common across Europe. GLS sees no need to reduce its sales volumes by spreading the mortgages around other lenders to manage project risk, and it likes to have a complete picture of the finances for the whole project. As the project proceeds, the mortgages are released in stages to pay the contractor. At the end the individuals own their individual homes.

Of the nearly 300 projects that the bank has financed it has never experienced a terminal default or a re-possession. Where groups have encountered problems – such as voids when members leave, or where building costs go over budget – the bank steps in early to provide advice and help find a solution (such as lower repayments for a short period of time). Experience has also shown that groups usually contact the bank well ahead of any potential problems. This approach to risk has resulted in only five missed monthly payments across all its projects since 1990.

THE ‘ESSLINGEN’ PARTNERSHIP MODEL

Background

The City of Esslingen am Neckar is located close to Stuttgart in southern Germany. In 2005 the council began to explore a new financial delivery model to support building groups looking to construct about 450 high density apartments on a 2.4 ha council-owned brownfield site known as ‘Grünen Höfe’.

Although the council had always intended to sell the site, it wanted to support a series of building groups to enable more affordable owner-occupied housing to be accessed by local people. However, there were two key delivery challenges: -

- The concept of building groups was largely unknown in the area at the time and there was a lack of demand from local people to join groups

- There was no financial support available to build the required basement car parking and greenspace areas that were identified in the site’s development brief.

How does the model work?

The council worked proactively with a local public-private housing developer Esslinger Wohnungsbau GmbH (EWB) who identified the project as a business opportunity.

To initiate the project the council agreed to seed fund the required basement car parking and greenspace areas. It also incentivised local building groups to come forward by offering to provide ‘options’ on parcels of land on a deferred payment basis.

Land prices were set at €378 per sq m with families with children offered a discount on the cost of the land (€2,000 for one child, €6,000 for two children and €12,000 for three children).

While groups were forming and buyers for the land were being secured EWB initiated a market appraisal and worked with local architects and engineers to develop a viable development proposal for the whole site. This also set out how the costs could be distributed to each of the building groups.

EWB also engaged with each building group to refine the proposals to suit their requirements and then entered into contract to build the homes for each group.

Where a group was initially short of members EWB agreed to take ownership of any unreserved homes and held these open for others to join during construction. If new members could not be recruited the contract allowed EWB to sell the homes as market housing on completion.

This approach enabled the project to start on site, reduce risk and helped groups secure the necessary finance. The seed funding that the council invested at the start of the project was repaid through land sales.

Judging success

The model has enabled several building groups to complete a series of affordable, high quality, energy efficient projects which have collectively raised the development quality and land values in the wider neighbourhood. Eight residential blocks (100 homes) have already been developed, including several ground floor commercial units. Six of these (64 homes) have been completed for building groups, including the following: -

- HORST (completed 2010) - a passive house project of 10 apartments (two to five bedrooms). Six of these were acquired by building group members at the start of the project, and the other four sold by EWB

- BLICKE (completed 2011) - 12 apartments (of two to five bedrooms) and a commercial unit. When construction started six of the homes had been reserved by building group members, and six were held by EWB. During the construction phase three additional group members came forward and the remaining three were sold on the open market

- HaGeF (completed 2012) - 13 apartments (two to three bedrooms) developed for a building group of older women. Three apartments were owner occupied and ten rented on a long lease by EWB. The project also includes a common room on the ground floor which serves as a meeting point for residents

- TEAM SPIRIT (completed 2013) - 11 apartments (two to four bedrooms) and a commercial unit. Nine of the apartments and the commercial unit were sold and occupied by members of the building group at the start of the project. The remaining homes were sold on the open market by the EWB

More projects are currently in development. The model has received widespread interest from a range of housing providers in the wider region and EWB has begun working with other councils to deliver similar outcomes. The success of the model has also convinced the City of Esslingen’s local politicians to bring more land forward for building groups.

The TEAM SPIRIT development in the City of Esslingen am Neckar

The TEAM SPIRIT development in the City of Esslingen am Neckar  The HaGeF project provides homes for a group of older women

The HaGeF project provides homes for a group of older women

Further Reading

The following Case Studies offer useful insight into the issues discussed in this Briefing Note:

read more

read more

read more

read more

read more

read more

read more

CREDITS

The NaCSBA Research & Development Programme is funded by the Nationwide Foundation and aims to promote the self-build and custom build sector as an affordable route into housing for a greater number of people in the UK.

For further information, please visit:

www.nacsba.org.uk or www.selfbuildportal.org.uk